It’s hard to escape any discussion of Wayfair these days. This isn’t surprising, as we witnessed history on June 21, 2018, when the U.S. Supreme Court overturned the physical presence standard in South Dakota v. Wayfair. And in doing so, overturned 51 years of precedent that had restricted states from imposing their sales tax obligations on out-of-state (“remote”) retailers who lacked a physical presence in their state.

Yes, this was indeed a momentous development – one that has dramatically changed the sales tax landscape in a very short time.

As important as the outcome of the decision, was the U.S. Supreme Court’s admission that Quill had been an “incorrect interpretation of the Commerce Clause” both as first formulated by the Bellas Hess and Quill courts as well as applied today and one which became “further removed from economic reality” each year. Calling Quill flawed on its own terms, the Wayfair Court held that: (1) the physical presence rule is not a necessary interpretation of the substantial nexus requirement; (2) Quill creates, rather than resolves, market distortions; and (3) Quillimposes the sort of arbitrary, formalistic distinction that the Court’s modern Commerce Clause precedents disavow.

It was, for many reasons, the expected decision. Justice Kennedy, who wrote the majority opinion on Wayfair, had been very clear in his 2015 opinion in Direct Marketing Association v. Brohl (which dealt with Colorado’s notification & reporting law), that the time had come for the U.S. Supreme Court to reconsider Quill. In 2016, South Dakota saw this as an invitation to present the Court with a case that challenged Quill and wasted no time enacting its economic nexus law. (For more on South Dakota’s economic nexus law, see this PrietoDion SALT Whitepaper)

Despite the many arguments the majority voiced for overturning Quill, Justice Roberts, who authored the dissenting opinion, made a valid point in his dissent. Even if he agreed that the prior Supreme Court decisions (National Bellas Hess and Quill) affirming the physical presence standard were wrongly decided, the Supreme Court’s majority decision to overturn Quill may have lessened Congress’ motivation to consider the issue. Does the Wayfair decision mean the U.S. Congress will be less likely, or more likely, to enact a federal remote seller legislation?

U.S. Judiciary Committee Holds Hearing to Examine Wayfair Decision

In an effort to further explore whether and what action the U.S. Congress should take, on July 24th the U.S. House Judiciary Committee held a Congressional hearing to examine the Wayfair decision and its ramifications for consumers and small businesses. Judiciary Committee Chairman, Bob Goodlatte (R-VA), a vocal proponent of a workable, Congressional solution was quick to issue a statement soon after the Wayfair decision was announced in which he emphasized his disappointment in the decision and called the Court’s reversal of Quill’s physical presence principle “a nightmare for American businesses and small online sellers.” He added that “the dominant issues under debate in this case involved policy, not law. The briefs filed with the Court were filled with discussions of economics, the efficacy of software, trends in the retail industry, and myriad other non-legal questions” and added that “Congress is the appropriate institution to resolve these policy questions, not the Supreme Court.“ In his opening statement at the July 24thhearing, he stated that “the Court could have left resolution of this issue to Congress, to which the Commerce Clause grants the ultimate authority to regulate interstate commerce.”

Federal Remote Seller Proposals

At the July 24th hearing there was testimony from parties stating that a Congressional solution was still needed to bring uniformity and parties stating that Congressional action was no longer required now that Wayfairhad been decided. (You can hear the entire Judiciary Committee hearing and read each witness’ testimony here.)

As of August 1st, four federal remote seller proposals have been introduced by the 115th U.S. Congress. Although the Judiciary Committee hearing did not focus on any one specific federal proposal (the idea was to explore whether Congressional action was still warranted) it should be noted that two of the federal proposals aim to limit states’ collection authority by bringing back the physical presence standard overturned by Wayfair. Given Chairman Goodlatte’s outspoken criticism of the Wayfairdecision, a key focus was reviewing whether Congressional action that would rein in the states newly expanded authority was needed.

In reviewing the four federal proposals, it should be noted that they focus on two opposite goals. Two of four proposals, the Marketplace Fairness Act of 2017 (S. 976) and Remote Transactions Parity Act of 2017 (H.R. 2193), would grant “collection authority” to states that simplify their sales tax administration (such as is required of Streamlined Sales Tax member states) and comply with other requirements detailed in the proposals. The other two federal proposals, the No Regulation Without Representation Act of 2017 (H.R. 2887) and the Stop Taxing Our Potential Act of 2018 (S. 3180) would limit Wayfair’simpact and states’ collection authority by codifying a physical presence standard.

Since the primary goal of the Marketplace Fairness Act (MFA) and the Remote Transactions Parity Act (RTPA) is the granting of “collection authority” to states – authority which would allow states to impose their sales tax collection obligation on remote sellers even if they had no physical presence in the state – it might seem that these proposals are no longer necessary post-Wayfair. In effect,because Wayfair removed the physical presence standard, Wayfair has already permitted states to have this same collection authority. However, post-Wayfair, states are free to adopt economic nexus standards that can vary from state to state. The MFA or RTFA would impose similar requisites on all states thus lessening the complexity created by states adopting a myriad of economic nexus rules.

The two other federal proposals, the No Regulation Without Representation Act and the Stop Taxing Our Potential Act (STOP), would prohibit a state from imposing a sales tax collection duty or information reporting obligation on a “person” who does not have a physical presence in the state. Both proposals define what constitutes a physical presence, as well as what activities would be considered a ‘di-minimus’ physical presence (which would be insufficient to be considered a physical presence that would allow a state to impose its tax collecting and remittance obligations on a remote seller). Under both proposals, commonly recognized direct activities, such as having a retail store, manufacturing operation, owing or leasing property or having employees in the state would be a nexus creating physical presence, but engaging marketing affiliates (which create nexus in states with click-through nexus laws) would be considered a ‘di-minimus’ physical presence.

Are States Rushing to Adopt Economic Nexus Too Quickly

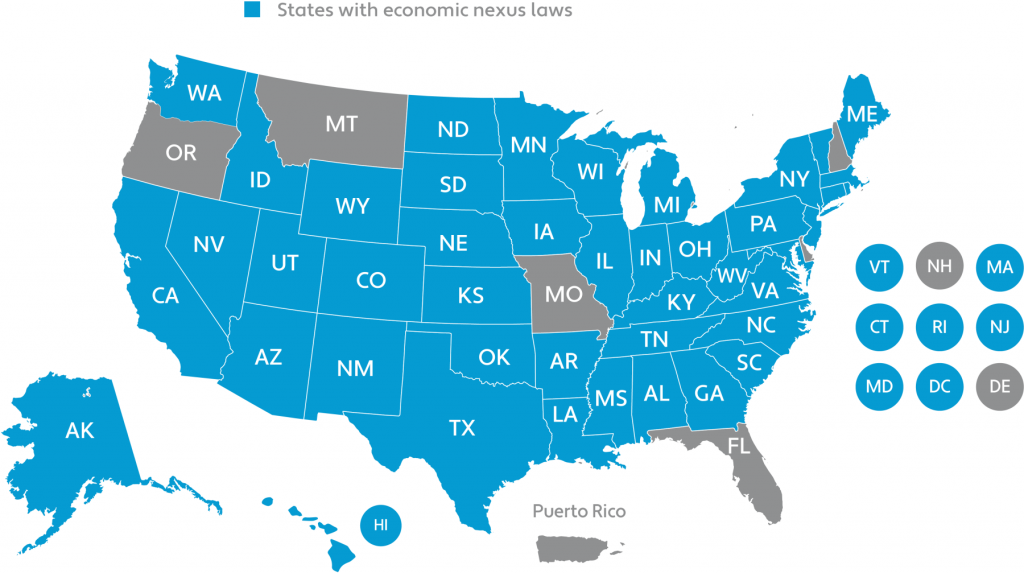

Prior to and after the decision was announced, I was asked about my thoughts on Wayfair. I noted in this “Reflections On The Supreme Court’s Reflections On Sales Tax” article by Peter Reilly, a contributor at Forbes.com, my concern that if the physical presence standard was reversed the flood gates would open and many more states would see this as an opportunity to enact South Dakota styled laws – focusing solely on revenue and transaction thresholds to assert sales tax nexus. And this is indeed what has occurred. As of September 1st,more than half of states in the country have adopted economic nexus. While some states have adopted economic nexus through legislation, others have done so by updating their existing regulations or drafting new economic nexus regulations, and yet others are simply adopting economic nexus through administrative policy. By the way, if you’re wondering which states have adopted economic nexus, see my blog article at SalesTaxSupport.com, “States Follow South Dakota: A By-State Guide on Economic Nexus.” Here you’ll find an Economic Nexus Chart that lists every state that has adopted economic nexus, the economic thresholds (sales and/or transactions in each state), the law’s effective date, as well as links to the different state websites, press releases, FAQs and other state resources where helpful information can be found.

In creating the Economic Nexus chart, I reviewed every bill, regulation and administrative policy document explaining the various states’ economic nexus provisions and can confirm that there is indeed a lack of uniformity. For instance, some states base their economic revenue threshold on taxable sales, others mention retail sales, others mention gross sales and others explicitly state that both taxable and exempt sales are to be considered in determining if the sales threshold has been exceeded. The revenue dollar amount also varies by state. While many states have adopted the same “more than $100,000 in sales” used in South Dakota, the revenue threshold in some states is as low as $10,000 and in others, as high as $500,000. Also, in some states, a remote seller must meet both the revenue and transactions thresholds, while in other states, meeting either the sales OR transactions threshold will trigger nexus. Additionally, in some states, the economic nexus law is tied into the state’s notification and reporting law. In these states, remote sellers that meet an economic nexus revenue threshold must either register to collect and remit or comply with the state’s notification and reporting law. Another area lacking uniformity is the period is used to measure when a remote seller meets the economic nexus thresholds. While many states use a prior or current calendar year measurement period, other states use a rolling “prior 12-month period” or “prior 4 quarters” period.

Sylvia’s Summation

On June 21, 2018, the U.S. Supreme overturned the physical presence standard first established in National Bellas Hess and re-affirmed in Quill. With the physical presence standard removed, states were free to adopt economic nexus. And states wasted no time – as of September 1st, more than half of the states in the country have adopted economic nexus. In his opening statement at the July 24th hearing, Chairman Goodlatte highlighted that “retailers should not be getting different answers from different states.” But with more and more states adopting economic nexus, “different answers from different states” is exactly what remote sellers are getting. Which brings us back to the question – is a federal solution still needed? It may very well be.

Like this post? Click on the “SHARE” link to Share It on Social Media

Are you an online retailer interested in a tax consultation? Submit a contact request or email Sylvia Dion at sylviadion@prietodiontax.com

About the Author: Sylvia F. Dion, CPA is the Founder and Managing Partner of PrietoDion Consulting Partners LLC, a State & Local Tax (SALT) Consulting firm providing comprehensive tax services to U.S. and International businesses. Sylvia’s 25 years of multi-faceted tax experience includes holding leadership positions with some of the highest regarded international accounting firms and providing SALT services to companies around the world. From 2011 through 2019, Sylvia also served as a contributor to the SalesTaxSupport* blogs, where she blogged on Internet Sales Tax and Economic Nexus, U.S. Sales Tax for Foreign Sellers and Massachusetts Sales Tax. Sylvia is also a speaker and author whose articles have been published by Bloomberg BNA and in other leading professional tax journals and is the author of “Minding Massachusetts,” a quarterly column published by Tax Analysts’ State Tax Notes. Sylvia is also fluent in Spanish. For more about Sylvia visit the her firm website at www.prietodiontax.com or www.sylviadioncpa.com. You can follow Sylvia on twitter and on Google+ and can contact Sylvia via e-mail at sylviadion@prietodiontax.com

*SalesTaxSupport was formerly a sales tax resource website which closed on March 1, 2019. Many of Sylvia’s posts previously published on SalesTaxSupport have been republished here at “The State and Local Tax ‘Buzz’ ” blog.